Both the Discover it Cash Back and the Citi Double Cash sit in the same corner of the market: no annual fee, straightforward cash rewards, and a wide pool of approved applicants. The difference is in how they pay you. One asks you to chase rotating bonus categories for a high rate; the other pays a steady rate on everything and asks nothing of you. Picking between them comes down to whether you enjoy a little quarterly effort or want a card you can forget about.

Discover it — rotating categories

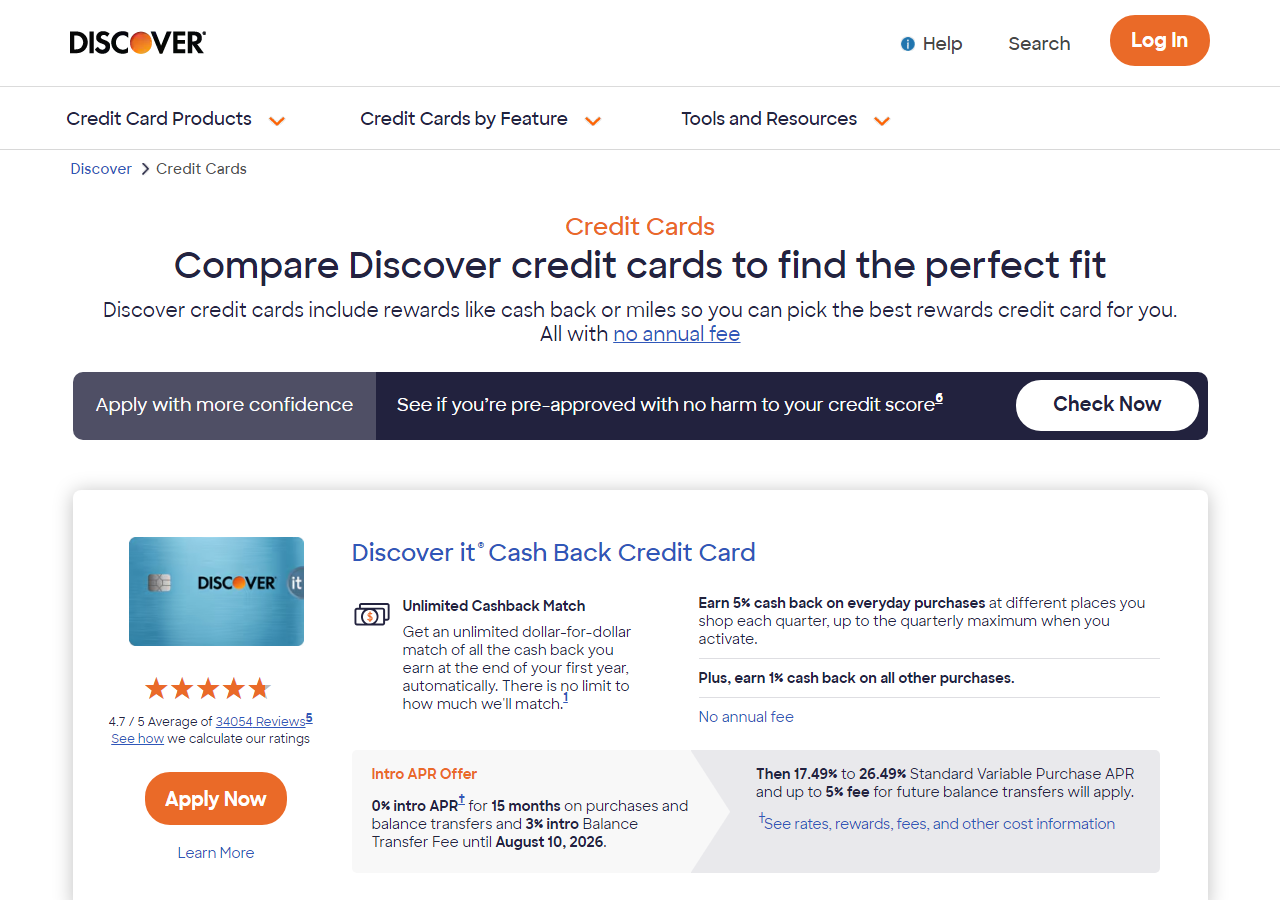

The Discover it Cash Back earns an elevated rate on categories that change every three months, on spending up to a quarterly cap, after you activate. Outside those categories and above the cap, purchases earn a flat baseline rate. Discover publishes the calendar of categories in advance, and past quarters have typically included things like grocery stores, restaurants, gas, and online retailers — but the exact lineup and cap shift year to year, so check the current calendar on Discover's site before you count on a category.

The catch most people forget is activation. You have to opt in each quarter, usually through the app, your online account, or an email link. If you forget, those purchases drop to the baseline rate. The card rewards a small amount of attention four times a year, and if you skip it, the headline rate quietly disappears.

This structure favors people who can steer spending toward the active category — buying groceries, fuel, or holiday gifts when those happen to be in season. If your spending is spread evenly across the year and you would rather not track a calendar, the rotating model leaves value on the table.

For a wider look at the lineup, see our best Discover credit cards for 2026 rundown.

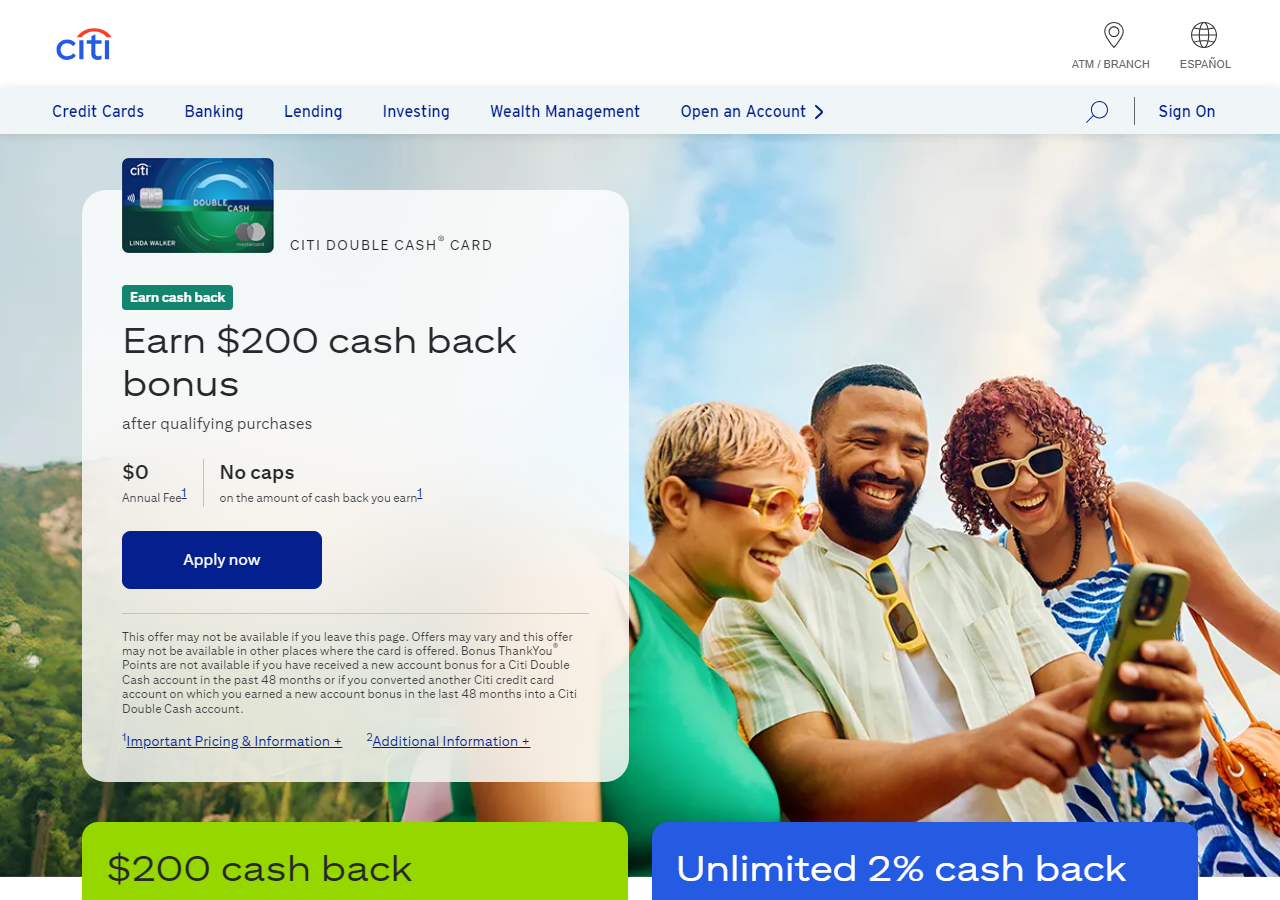

Citi Double Cash — flat 2%

The Citi Double Cash takes the opposite approach. It pays a flat rate on everything — split into a portion when you buy and a second portion when you pay off those purchases. There are no categories to activate, no calendar to watch, and no caps to track on the base earning. You swipe, you pay your bill, and the rewards add up.

The "pay your bill" half is worth underlining: you earn the second portion as you pay down the balance, which means carrying a balance and paying interest works against the whole point of the card. Used the way it's designed — paid in full each month — it delivers a solid, predictable return on every dollar regardless of what you buy.

This card suits people whose spending is varied or unpredictable, or who simply don't want a system. Rent-adjacent bills, medical costs, one-off purchases, everyday errands — all of it earns the same flat rate. You can read more in our best Citi credit card guide.

First-year cashback match

Discover has historically run a first-year incentive: at the end of your first 12 months, it matches the cash back you earned during that year. There is no separate spending threshold to hit and no cap mentioned on the match itself in past versions — but offers change, so confirm the current terms on Discover's site before you apply.

If that match is in effect when you apply, it changes the first-year math meaningfully. A doubled rotating rate during a strong category, plus a doubled baseline on everything else, can outpace a flat-rate card for the first year specifically. The key word is "first year" — the match is a one-time event, not an ongoing rate.

Citi's value proposition does not lean on a first-year match. Its strength is consistency over many years rather than a front-loaded bonus. When you compare the two, separate the first-year picture from the long-run picture; they can point to different winners.

- First year, if a match applies: Discover can come out ahead, especially if you hit the bonus categories.

- Year two onward: the comparison resets to rotating-plus-activation versus flat-rate-no-effort.

Foreign transaction fees

If you travel outside the United States or buy from merchants that process in another currency, foreign transaction fees matter. Discover has generally not charged a foreign transaction fee on its cards, which is unusual and useful abroad — though Discover's overseas acceptance is narrower than networks like Visa and Mastercard, so it may not be taken everywhere you go.

The Citi Double Cash, like many flat-rate cash cards, has historically charged a foreign transaction fee on purchases made abroad, which erodes the flat reward rate on those specific transactions. Neither of these cards is built as a dedicated travel card, so for frequent international spending you may want a separate no-foreign-fee travel card and keep these two for domestic use.

| Feature | Discover it Cash Back | Citi Double Cash |

|---|---|---|

| Annual fee | None | None |

| Rewards structure | Rotating bonus categories (activate quarterly) + flat baseline | Flat rate on everything (earn at purchase + at payment) |

| Effort required | Quarterly activation, category tracking | None beyond paying in full |

| First-year incentive | Cashback match has been offered (confirm current terms) | No first-year match |

| Foreign transaction fee | Typically none | Typically charged |

| Network reach abroad | Discover — narrower acceptance | Mastercard — wide acceptance |

Exact fees and terms vary by version and over time, so verify each item on the issuer's site before applying.

Which no-fee card to pick

There's no universal winner — the better card depends on how you spend and how much effort you're willing to spend chasing rewards.

- Pick Discover it if you'll actually activate each quarter, you can route spending into the active categories, and a possible first-year match appeals to you.

- Pick Citi Double Cash if you want a set-and-forget flat rate, your spending is spread across categories, and you value never thinking about a calendar.

- Hold both if you qualify: use Discover for active bonus categories and the Double Cash for everything else. Two no-annual-fee cards can cover more of your spending at a higher blended rate.

Whatever you choose, the rewards only make sense if you pay the statement in full every month. Interest charges on a carried balance will dwarf a few percent of cash back on either card.

Common questions

Do I have to activate the Discover it categories every quarter?

Yes. The elevated rate only applies after you opt in for that quarter, typically through Discover's app or website. Purchases in the bonus category before you activate earn the baseline rate instead.

Does the Citi Double Cash really pay rewards in two parts?

That's the design: a portion when you make the purchase and a second portion when you pay it off. Paying your balance in full each month is how you collect the full flat rate without giving it back in interest.

Is the Discover cashback match guaranteed?

It has been a recurring first-year offer, but issuer promotions change. Check Discover's current application page to confirm whether the match is available and what its terms are before you apply.

Can I use either card easily when traveling abroad?

Discover often skips foreign transaction fees but has narrower acceptance overseas, while the Double Cash runs on a widely accepted network but has typically charged a foreign fee. For heavy international spending, a dedicated no-foreign-fee travel card is usually the better tool.

Last updated: June 2026. Rates, fees, and issuer rules change — confirm current terms before you apply or transfer a balance. This is general information, not personal financial advice.

Tired of receiving your unsolicited mail, time for you to cease sending your mail. If I need a credit card I will ask for it on my own time.

hey there.. please call capital one at 1-877-383-4802 and tell them you would like your information removed from their system and no more mailings