Discover keeps its card menu short on purpose. Instead of a dozen overlapping products, you get a rotating-category cash back card, a flat-rate version, a travel-focused option, a student line, and a secured card for people building or repairing credit. Because Discover both issues the cards and runs its own payment network, the rewards and the customer experience tend to feel consistent across the lineup. This guide walks through who each Discover card fits, how the rotating 5% categories and activation work, where the network is accepted, and how to pair a Discover card with a second issuer so you are not leaving rewards on the table.

Discover it Cash Back lineup

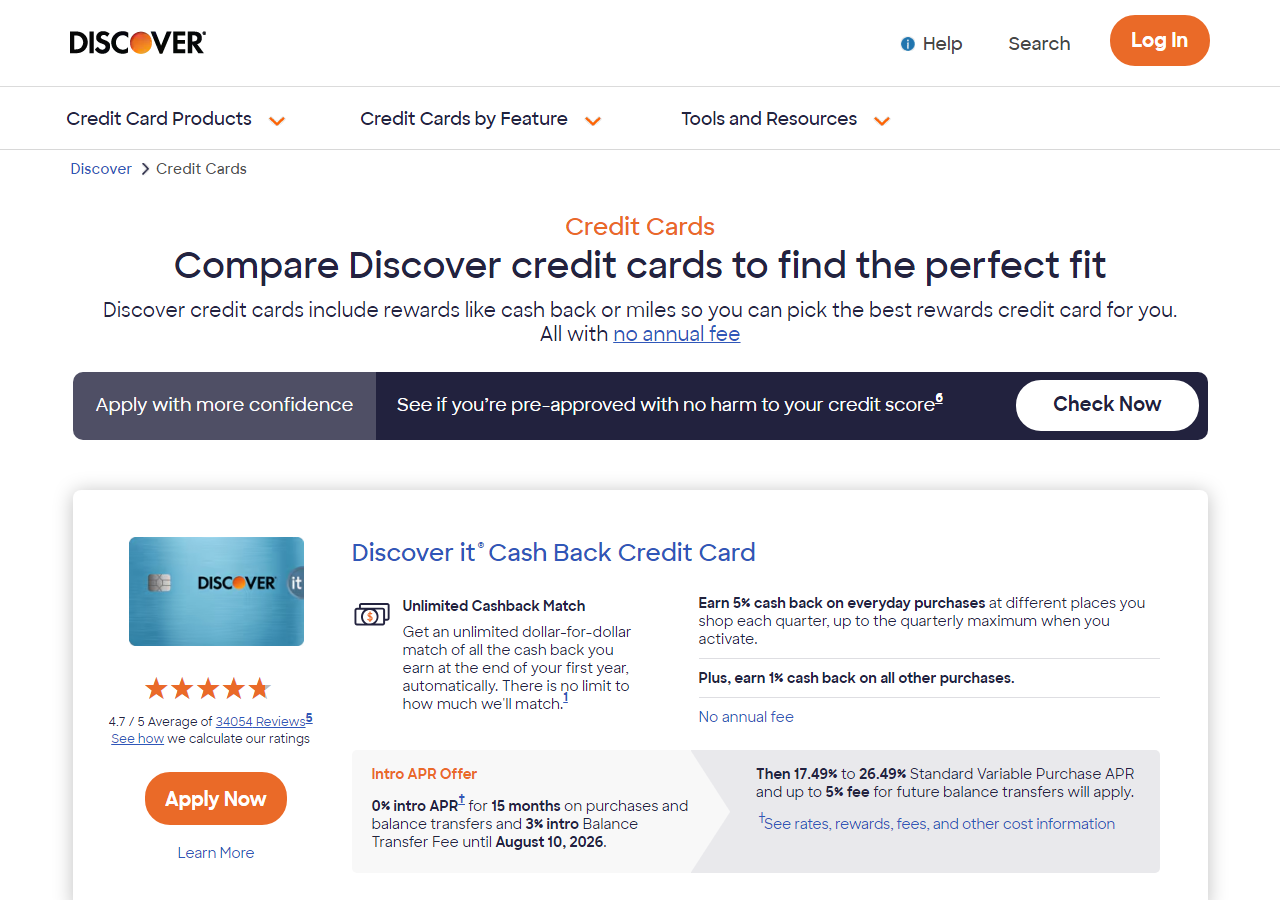

The core of the family is the Discover it Cash Back card. It earns an elevated cash back rate in categories that rotate each quarter, plus a flat rate on everything else, with no annual fee. The headline feature for new cardholders is Discover's first-year match: at the end of your first year, Discover automatically matches the cash back you earned. Discover has run this offer for several years, but match terms can change, so confirm the current offer on the issuer site before you apply.

A few siblings round out the menu:

- Discover it Chrome — a flat-category earner (gas and dining historically) for people who do not want to track rotating categories or remember to activate.

- Discover it Student Cash Back / Chrome — student versions with the same structure, aimed at first-time cardholders.

- Discover it Miles — a travel card that earns flat miles on every purchase, with a first-year miles match instead of cash back.

- Discover it Secured — a deposit-backed card for building or rebuilding credit, covered in its own section below.

None of these charge an annual fee, and Discover does not charge a foreign transaction fee — a real plus if you travel, even though acceptance abroad is a separate question we cover later.

Rotating categories and activation

The Discover it Cash Back card pays its top rate only in the quarter's bonus categories, and only up to a spending cap each quarter. Spending above the cap, and all spending outside the categories, earns the base flat rate. Typical categories over the years have included grocery stores, restaurants, gas stations, and online retailers, but the exact lineup is published by quarter — check Discover's category calendar rather than assuming.

You have to activate

This is the step people miss. The bonus rate does not apply automatically. You must activate the quarter's categories, and purchases before activation earn only the base rate. Activation takes a minute through your online account or the mobile app, and you can usually do it any time during the quarter — but earlier is better so you do not lose bonus weeks. If you want a walkthrough of the sign-in and activation flow, see how to activate a Discover card on discover.com.

Practical habits that help:

- Set a recurring calendar reminder for the first day of each quarter to activate.

- Route category spending (groceries, gas, dining) to the Discover card only after you have activated.

- Watch the quarterly cap; once you hit it, switch that spending to a flat-rate card.

If tracking categories sounds like work, the Chrome or Miles versions, or a flat-rate card from another issuer, may earn you more in practice than a 5% card you forget to activate.

Discover secured for rebuilding

The Discover it Secured card is one of the more useful tools for someone with thin or damaged credit. You put down a refundable security deposit that sets your credit line, and you use the card like any other. Unlike many starter cards, the secured version still earns cash back in a couple of everyday categories plus a base rate, and Discover has historically extended the first-year cash back match to it as well — verify that on the application page.

What makes it a rebuilding card rather than a dead end is the graduation path: Discover periodically reviews secured accounts and may return your deposit and move you to an unsecured card if you manage the account responsibly. To make that happen:

- Keep your balance low relative to your limit and pay the statement in full.

- Never miss a due date — payment history is the largest factor in your score.

- Let the account age; closing it early erases the progress.

Because the card reports to the major credit bureaus, on-time use builds the same history a regular card would. If you are still learning how that history is weighted, our comparison of Discover it and Citi Double Cash shows how a rebuilt profile can later qualify for stronger flat-rate cards.

Discover acceptance vs Visa/Mastercard

Discover runs its own network, which is the source of both its strengths and its main limitation. Inside the United States, acceptance is broad — the vast majority of merchants that take cards take Discover, and you will rarely be turned away at chains and major retailers. The gaps tend to show up at small independent merchants and, more noticeably, when you travel abroad.

Here is a simplified comparison of what matters for everyday use:

| Factor | Discover | Visa / Mastercard |

|---|---|---|

| U.S. acceptance | Very wide; occasional small-merchant gaps | Near-universal |

| International acceptance | Spotty in some regions; better via partner networks (e.g., Diners Club) | Broad worldwide |

| Foreign transaction fee | None on Discover cards | Varies by card |

| Annual fee on entry cards | $ 0 | $ 0 on many, varies |

The takeaway: Discover is an excellent domestic card, but if you travel internationally often, do not make it your only card. Carry a widely accepted Visa or Mastercard as a backup so an acceptance gap never strands you.

Pairing Discover with other issuers

Discover works best as part of a small two-card system rather than a do-everything card. The rotating 5% covers a slice of your spending well, but it leaves a lot of purchases earning only the base rate. A clean pairing fixes that.

A common setup:

- Discover it Cash Back for the activated bonus categories each quarter, up to the cap.

- A flat-rate card (for example, a 2% cash back card from another issuer) for everything outside the categories and above the cap.

- A widely accepted travel card if you go abroad, so you always have a network that works.

This keeps the logic simple: category spending on Discover after activation, everything else on the flat-rate card. You capture the high rate where it exists without micromanaging five cards. If you want to see how that base layer holds up against Discover's own flat earning, the Discover it vs. Citi Double Cash breakdown is a good next read.

Common questions

Do I have to activate Discover's 5% categories every quarter?

Yes. The bonus rate is not automatic. You activate each quarter through your online account or the app, and purchases made before you activate earn only the base rate. Set a reminder for the start of each quarter so you do not miss bonus weeks.

Is the Discover first-year cash back match guaranteed?

It has been a long-running offer, but it is still an offer that Discover sets and can change. Always confirm the current match terms on the Discover application page before you apply, rather than relying on past years.

Is Discover accepted everywhere?

In the U.S., acceptance is very wide, with only occasional gaps at small independent merchants. Internationally it can be spottier than Visa or Mastercard, so keep a second, widely accepted card for travel. Discover cards charge no foreign transaction fee, which helps when they are accepted.

Can the Discover it Secured card become a regular card?

Yes. Discover periodically reviews secured accounts and may refund your deposit and upgrade you to an unsecured card when you use the account responsibly — paying on time and keeping balances low. Keep the account open and active to let that review happen.

Last updated: June 2026. Rates, fees, and issuer rules change — confirm current terms before you apply or transfer a balance. This is general information, not personal financial advice.

Tired of receiving your unsolicited mail, time for you to cease sending your mail. If I need a credit card I will ask for it on my own time.

hey there.. please call capital one at 1-877-383-4802 and tell them you would like your information removed from their system and no more mailings