If a big share of your spending happens at restaurants, bars, and takeout counters, a card that pays extra on dining can be one of the easiest wins in your wallet. The catch is that "dining" is not a single, obvious category. Whether a purchase earns your bonus rate depends on how the merchant is classified, not on whether you think of it as eating out. This guide explains how dining rewards actually work and looks at three cards people reach for most: Capital One Savor, the American Express Gold Card, and Chase Freedom Flex. Specific bonus offers and earn rates change, so confirm current terms on each issuer's page before you apply.

How dining categories code

Card networks tag every merchant with a Merchant Category Code (MCC). When you tap or swipe, the network reads that code and your card decides whether the purchase counts as dining. A sit-down restaurant, a fast-food window, a bar, and a coffee shop usually code as restaurants, so they trigger a dining bonus. The trouble starts at the edges.

- Grocery store cafes and prepared-food counters often code as grocery, not dining.

- Hotel restaurants and stadium concessions may code under the parent business (lodging or entertainment) instead of dining.

- Catering, food trucks, and pop-ups can code unpredictably depending on the payment processor they use.

You can't see the MCC before you pay, and you generally can't change it. The practical move is to check your statement after the fact: each issuer lists how a transaction was categorized, so you can learn which of your regular spots earn the bonus and which quietly fall to the base rate.

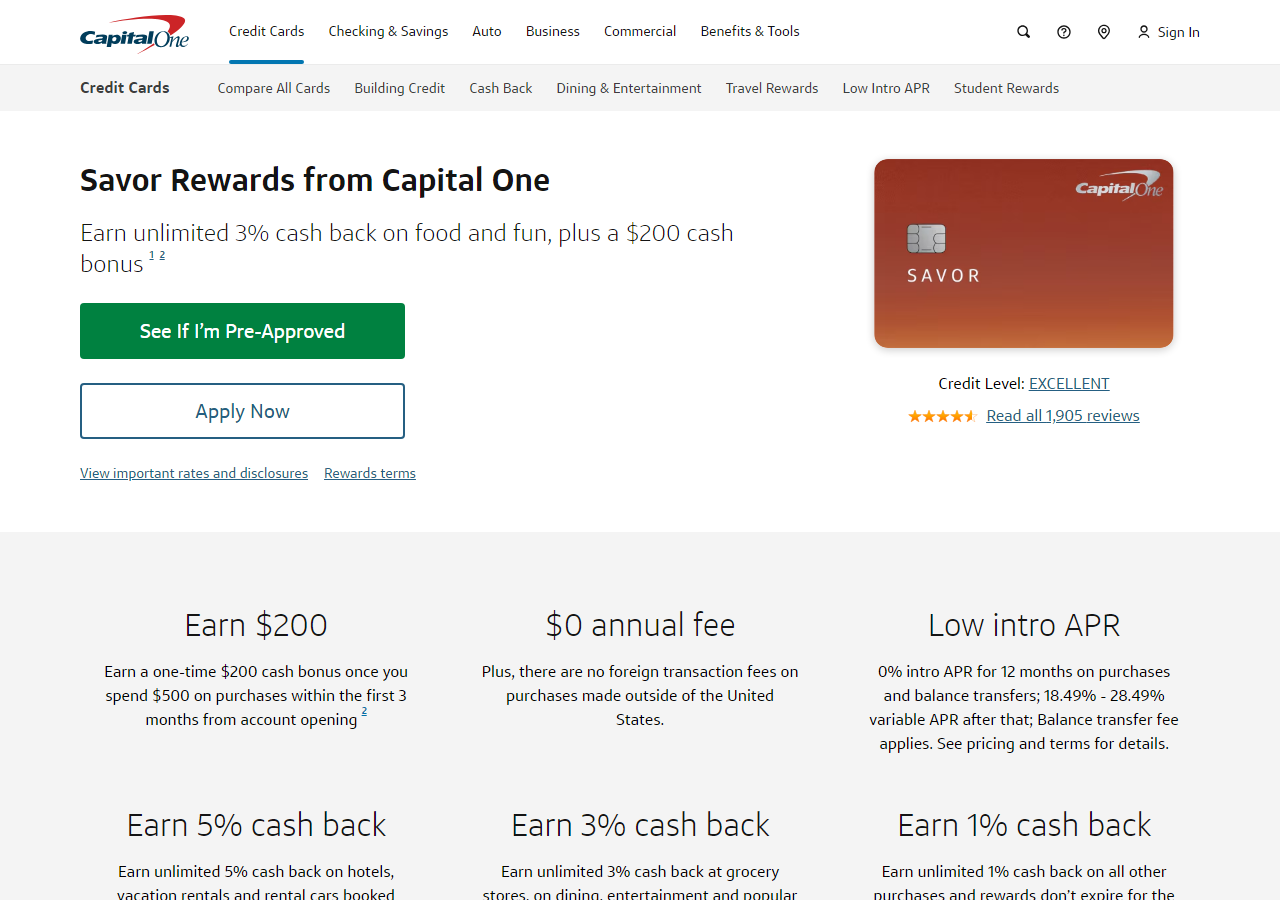

Capital One Savor and SavorOne

The Savor line is built around dining and entertainment. Capital One has shuffled its Savor and SavorOne branding over time, so the exact names and any annual fee depend on what's currently offered — check the issuer page for the live version. The appeal is consistent: strong cash back on restaurants plus entertainment and, on most versions, grocery stores, which makes it a flexible everyday earner rather than a narrow dining-only card.

Cash back is simple to use, with no points to transfer or redeem through a portal. That's a fair trade if you'd rather not manage a rewards program. If you also spend on travel, it's worth weighing the Savor against Capital One's miles cards; the Capital One Venture X vs Savor comparison walks through when flat cash back beats transferable miles.

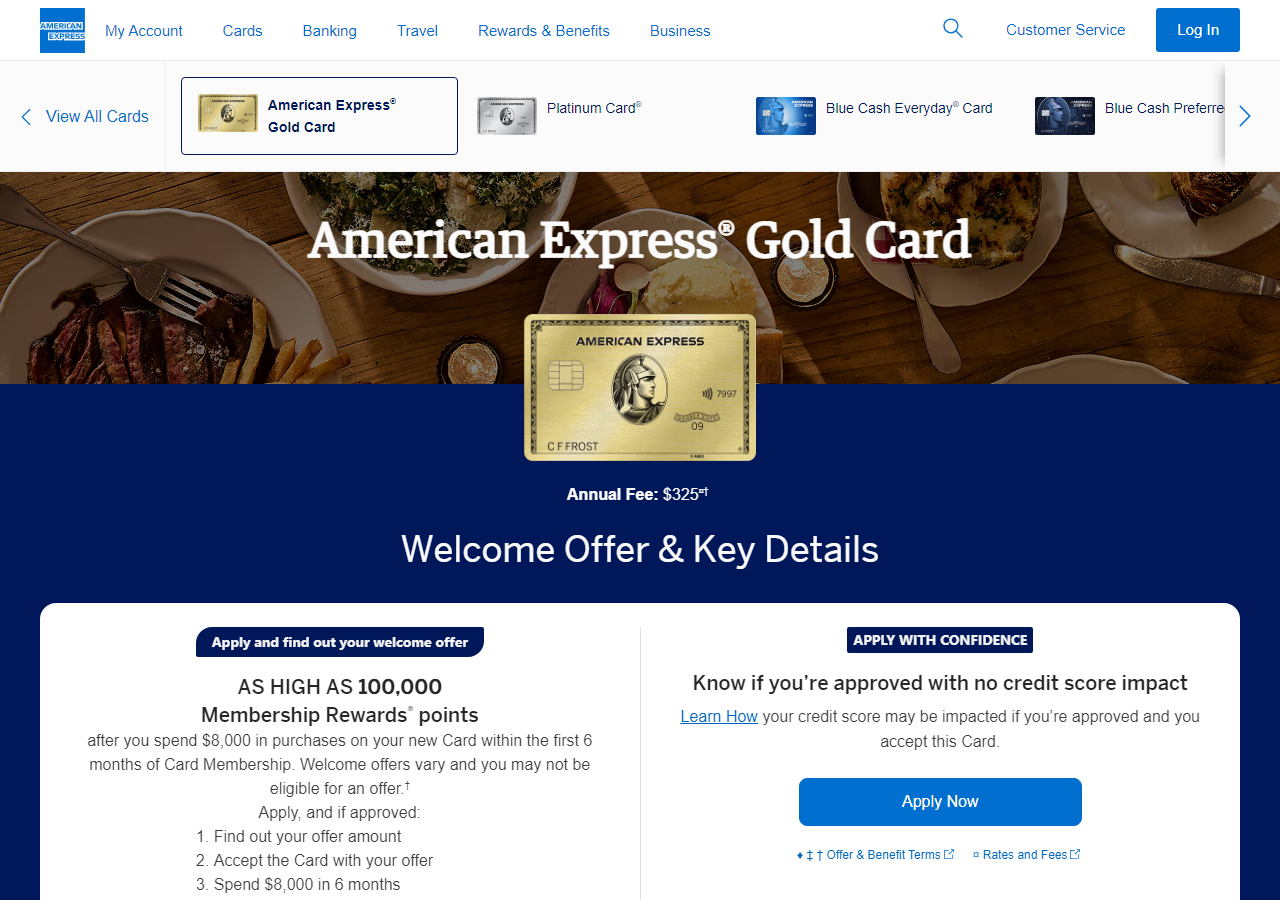

Amex Gold for restaurants

The American Express Gold Card is the heavy hitter for people who eat out often. It earns Membership Rewards points at an elevated rate on restaurants worldwide and on U.S. supermarkets, usually up to an annual spending cap on the supermarket category. Membership Rewards can be transferred to airline and hotel partners, which is where points-focused users squeeze out extra value beyond a flat cash-back rate.

The Gold Card carries a meaningful annual fee, partly offset by dining and other statement credits that come with enrollment and conditions. Those credits only help if you'd use the partner services anyway; otherwise they're a discount on things you don't need. To see where the Gold sits against other Amex options, the best American Express card overview compares the lineup by fee and earning style. As always, confirm the current fee, credits, and earn rates on the Amex site before applying.

Chase Freedom Flex 3% dining

Chase Freedom Flex takes a different angle: no annual fee, with an ongoing elevated rate on dining and drugstores plus rotating quarterly categories you activate. The dining bonus applies year-round, so it's a solid no-fee option if you want extra back on restaurants without paying for the privilege.

Freedom Flex earns Ultimate Rewards points. On its own those redeem for cash back, but if you also hold a Sapphire card, you can pool points and unlock transfer partners — a common way to stretch a no-fee card's value. The rotating categories require you to remember to activate each quarter, which is the main maintenance cost of the card.

| Card | Reward type | Annual fee | Best for |

|---|---|---|---|

| Capital One Savor | Cash back | Varies — check issuer | Simple dining + entertainment cash back |

| Amex Gold | Transferable points | Higher fee, offset by credits | Frequent diners who use points for travel |

| Chase Freedom Flex | Points / cash back | No annual fee | No-fee dining earner with rotating bonuses |

Delivery apps and card coding

Food delivery is where dining rewards get slippery. When you order through an app, the purchase usually codes to the platform's processor, not to the restaurant. Sometimes that processor codes as a restaurant and your dining bonus applies; other times it codes as a service or general merchant and you earn only the base rate.

- Ordering directly from a restaurant's own site or paying in person is the most reliable way to hit the dining category.

- Some cards include delivery credits or partnerships with specific apps; these are credits, separate from how the MCC codes, and they depend on enrollment.

- Check a small test order's statement entry before assuming your favorite app earns the bonus.

None of these cards guarantees that every delivery order earns the dining rate, so don't pick a card on delivery alone. Treat in-person and direct-order dining as the dependable bonus, and treat app coding as a bonus you verify rather than expect.

Common questions

Does fast food count as a restaurant for rewards?

Usually yes. Most fast-food chains and drive-throughs code as restaurants, so they typically earn the dining bonus. Some locations run through grocery or convenience-store processors and won't, so check your statement if a specific spot matters to you.

Why didn't my dining card earn the bonus at a particular place?

Almost always because the merchant codes under a different category — a hotel, a grocery store, an entertainment venue, or a delivery platform. The issuer pays based on the MCC, not on the type of food, and you can see the assigned category on your statement.

Is a cash-back dining card or a points card better?

Cash back is simpler and good if you won't manage a rewards program. Transferable points like Amex Membership Rewards or Chase Ultimate Rewards can be worth more if you redeem them for travel, but only if you actually do. Match the card to how you'll redeem, not to the highest headline rate.

Do delivery apps earn dining rewards?

Sometimes. It depends on how the app's payment processor codes the charge, which varies by platform and region. Ordering directly from the restaurant is the most reliable way to earn the dining category, and any app-specific credits are separate perks tied to enrollment.

Last updated: June 2026. Rates, fees, and issuer rules change — confirm current terms before you apply or transfer a balance. This is general information, not personal financial advice.

Tired of receiving your unsolicited mail, time for you to cease sending your mail. If I need a credit card I will ask for it on my own time.

hey there.. please call capital one at 1-877-383-4802 and tell them you would like your information removed from their system and no more mailings