The American Express Gold Card and the Platinum Card are both premium rewards cards, but they reward very different spending. Gold leans into everyday dining and groceries; Platinum is built around flights, lounges, and travel status. Picking between them comes down to where your money actually goes each month and how many statement credits you will realistically use. Below is how the two compare so you can choose one — or decide whether holding both makes sense.

Annual fees compared

Both cards carry an annual fee, and the Platinum fee is meaningfully higher than the Gold fee. Amex has adjusted these fees over time, so confirm the current numbers on the issuer site before you apply. The headline fee is only half the story: each card offsets part of its cost with statement credits, and those credits are only worth the full amount if your habits line up with them.

A useful way to think about it: write down the fee, then subtract only the credits you would have spent money on anyway. What remains is your real out-of-pocket cost. Do that for both cards and the comparison gets much clearer.

| Feature | Amex Gold | Amex Platinum |

|---|---|---|

| Annual fee | Lower (check issuer) | Higher (check issuer) |

| Best for | Dining and groceries | Flights and lounges |

| Lounge access | No | Yes (Centurion, Priority Pass, etc.) |

| Strongest multipliers | Restaurants, U.S. supermarkets | Flights and prepaid hotels via Amex Travel |

| Credit structure | Dining/food-focused credits | Travel, lifestyle, and retail credits |

Card terms shift, so treat the rows above as a framework rather than a quote. For a wider look at the lineup, see our overview of the best American Express card options.

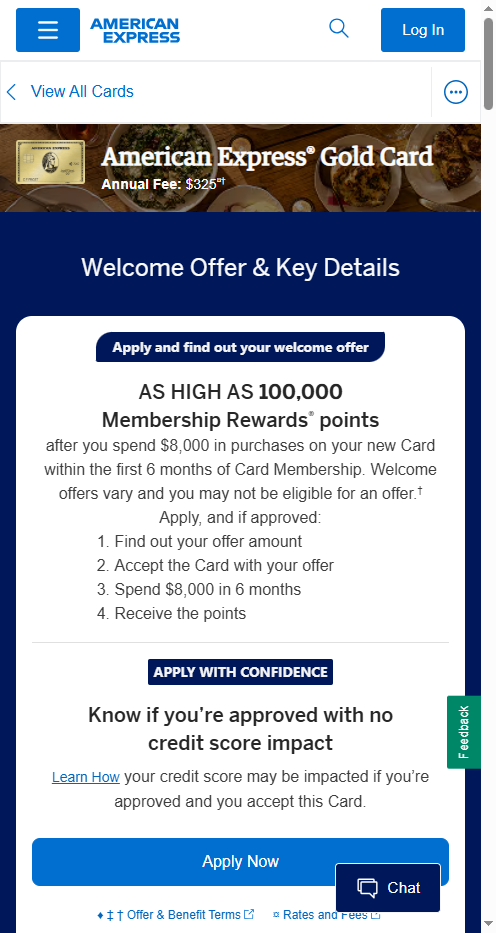

Gold — dining and supermarket multipliers

The Gold Card earns elevated rewards at restaurants and at U.S. supermarkets, usually up to an annual cap on the grocery category. That makes it a strong fit for households that cook, order in, and eat out regularly. If a large share of your monthly spend is food, Gold's earn rate can quietly outpace cards with a higher headline fee.

Gold also carries food-oriented statement credits — historically things like dining and delivery credits that arrive in monthly increments. Monthly credits only help if you remember to use them, so they reward people with predictable habits and hurt people who forget. If your grocery and restaurant spending is heavy, the Gold Card pairs naturally with our guide to the best credit cards for groceries in 2026.

- Elevated points at restaurants worldwide.

- Elevated points at U.S. supermarkets, typically up to an annual spending cap.

- Food and dining statement credits paid in monthly chunks (use-it-or-lose-it).

- No airport lounge access.

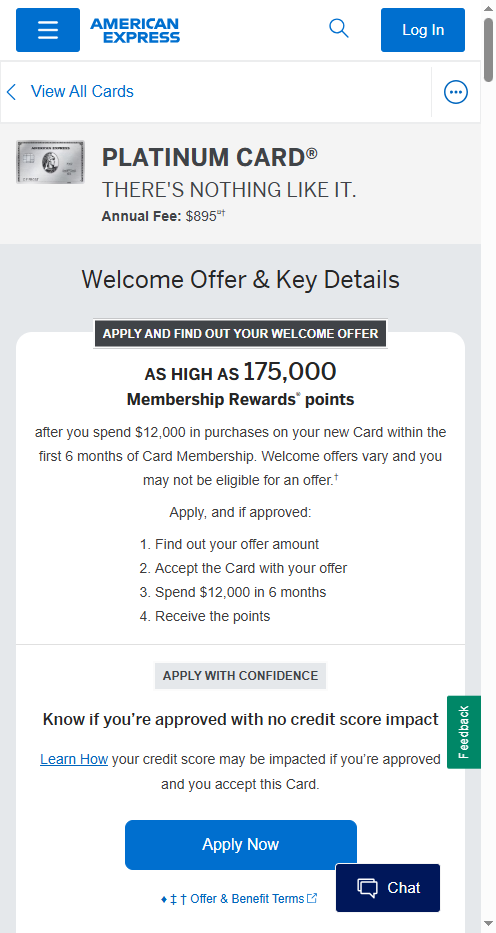

Platinum — travel perks and lounges

The Platinum Card is a travel card first. Its signature benefit is broad lounge access, including Amex Centurion Lounges, Priority Pass enrollment, and partner networks. For frequent flyers, that access plus elevated earning on flights and prepaid hotels booked through Amex Travel is the core of the value.

Platinum layers on travel and lifestyle credits, airline incidental credits, hotel benefits, and often hotel-program elite status. The catch is that several of these credits are narrow — tied to specific airlines, brands, or merchants — so they are only worth their face value if they match how you already spend. If you fly a few times a year and value the lounge and status perks, Platinum can justify its fee; if you mostly stay home, much of it sits unused. It fits the profile we describe in our roundup of the best travel credit cards for 2026.

- Lounge access across Centurion, Priority Pass, and partner lounges.

- Elevated points on flights and prepaid hotels booked through Amex Travel.

- Annual travel, hotel, and lifestyle statement credits (often brand-specific).

- Hotel elite status and travel protections.

Credits you must actually use

Both cards are sold partly on the idea that their credits "cancel out" the fee. That is only true for credits you would have spent on regardless. A monthly dining credit is easy to use if you already order food often; an airline incidental credit is wasted if you do not fly that airline. Before applying, list each card's credits and mark them as certain, maybe, or never for your life.

- Write down every credit and its dollar value.

- Cross out any credit you would not naturally spend money on.

- Add up what remains — that is your effective credit value.

- Subtract it from the annual fee to get your real cost.

Many credits reset monthly or quarterly rather than annually, so they cannot be saved up. People who track these well come out ahead; people who treat the card as "set and forget" often leave money on the table. Be honest about which group you are in.

Gold vs Platinum — decision checklist

Run through these questions and the answer usually becomes obvious:

- Where does most of my spending go? Food and groceries point to Gold; flights and hotels point to Platinum.

- How often do I fly? A few trips a year make lounge access and travel credits worthwhile; rare travel does not.

- Will I use monthly credits? If you forget recurring perks, Gold's lower fee is the safer bet.

- Do I want status and protections? Hotel elite status and travel coverage lean Platinum.

- Is the higher fee comfortable? Only keep Platinum if its perks clear its fee for your habits, not on paper.

Some people hold both: Gold for daily dining and grocery earning, Platinum for travel and lounges. That stacks two annual fees, so it only makes sense when each card's perks pay for themselves on their own. If you are unsure, start with the one that matches your largest spending category and add the second later if the gap is real.

Common questions

Is the Amex Gold or Platinum better for everyday spending?

Gold is usually the stronger everyday card because it earns elevated rewards on dining and U.S. supermarkets, which are common monthly categories. Platinum's best earning is concentrated in travel booked a certain way, so it shines less on routine purchases.

Does the Amex Gold Card include airport lounge access?

No. Lounge access is a Platinum benefit. If lounges matter to you, that is one of the clearest reasons to choose Platinum over Gold.

Can I have both the Gold and Platinum cards?

Yes, you can hold both, but you pay two annual fees. It only makes sense if your spending and travel are heavy enough that each card's rewards and credits justify its own fee.

Are the statement credits really worth the annual fee?

Only the credits you would have spent on anyway count toward offsetting the fee. Many credits are monthly or brand-specific, so map each one to your actual habits before assuming they cancel out the cost. Offers and credit details change — check the issuer site for current terms.

Last updated: June 2026. Rates, fees, and issuer rules change — confirm current terms before you apply or transfer a balance. This is general information, not personal financial advice.

Tired of receiving your unsolicited mail, time for you to cease sending your mail. If I need a credit card I will ask for it on my own time.

hey there.. please call capital one at 1-877-383-4802 and tell them you would like your information removed from their system and no more mailings