A travel credit card earns its keep in two ways: the rewards you collect on everyday spending and the credits, lounge access, and protections that come bundled with the annual fee. The trick is matching the card to how you actually travel, not to the marketing. Someone who flies twice a year wants a different card than someone who lives in airport lounges. Below is how the main U.S. travel cards stack up in 2026, what the fees buy you, and how to decide whether paying for a premium card makes sense.

What makes a travel card worth the annual fee

Most travel cards charge an annual fee, and the question is always whether the benefits return more than that fee in real value you will use. A few things move the math:

- Statement credits. Travel credits, hotel credits, or airline incidental credits only count if you would have spent that money anyway. A credit you have to chase or that expires unused is worth nothing.

- Lounge access. Valuable if you spend real time in airports, close to worthless if you mostly catch short domestic hops and never linger.

- Transfer partners. Cards that let you move points to airline and hotel programs can stretch a point further than a fixed cash-back rate, but only if you learn the programs.

- Protections. Trip delay, baggage, and rental car coverage can save a bad trip, and they are easy to overlook until you need them.

Run the numbers honestly. Add up the credits you will genuinely use, subtract the annual fee, and see what is left before you factor in points. If the card is underwater before you earn a single point, it is the wrong card for you.

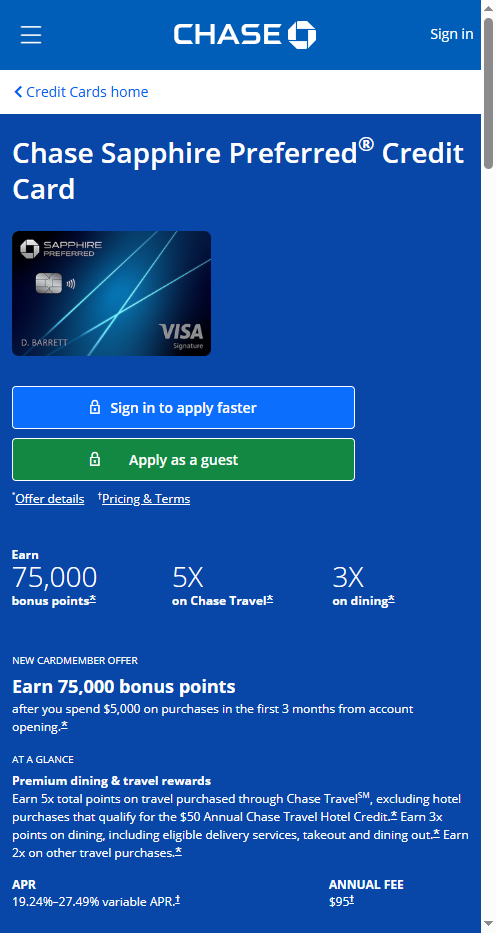

Chase Sapphire Preferred and Reserve

The two Sapphire cards anchor Chase's travel lineup and sit at different price points. The Preferred is the mid-tier card: a moderate annual fee, solid earning on travel and dining, and access to Chase's transfer partners. It fits travelers who want flexible points without a premium-tier bill.

The Reserve sits above it with a higher annual fee, a travel credit that offsets part of that fee, lounge access, and stronger trip protections. It rewards people who travel often enough to use the credits and lounges every year. If you are deciding between the two tiers, our deeper breakdown in Chase Sapphire Preferred vs Reserve 2026 walks through the net annual cost for each.

Both cards waive foreign transaction fees and earn transferable points, which is the main reason travelers reach for the Sapphire family over a flat cash-back card. Exact fees, credits, and earning rates change, so confirm the current terms on Chase's site before you apply.

Amex Platinum — lounges and flights

The American Express Platinum is built for frequent flyers who value airport experience over simplicity. Its annual fee is among the highest of any consumer card, and it offsets that with a bundle of statement credits plus broad lounge access, including Amex's own Centurion lounges and Priority Pass.

The catch is that the Platinum's value is spread across many separate credits, each with its own rules and enrollment. If you do not use the airline, hotel, and other credits, the card can cost you more than it returns. It works best for travelers who fly enough to live in lounges and who will actually claim each credit rather than let them lapse.

If your spending leans toward dining and groceries rather than flights, the Amex Gold may fit better than the Platinum. We compare the two in Amex Gold vs Platinum 2026. One acceptance note: Amex coverage is excellent at major travel merchants but can be thinner at smaller shops abroad, so carry a Visa or Mastercard as backup.

Capital One Venture X — credits and simplicity

The Venture X is the simplest of the premium travel cards. It carries a mid-premium annual fee, gives a travel credit and lounge access, and earns a flat, easy-to-understand rate on every purchase plus a higher rate on travel booked through Capital One. You do not have to juggle a dozen separate credits to come out ahead.

That simplicity is the selling point. For travelers who want premium perks without managing a spreadsheet of credits, the Venture X often nets out favorably once the annual travel credit is applied. Capital One miles transfer to airline and hotel partners, and the card has no foreign transaction fee. Confirm current credits and lounge details on Capital One's site, since lounge networks and credit amounts shift over time.

| Card | Tier | Best for | Lounge access | Foreign transaction fee |

|---|---|---|---|---|

| Sapphire Preferred | Mid | Flexible points, lower fee | No | None |

| Sapphire Reserve | Premium | Frequent travelers wanting credits and protections | Yes | None |

| Amex Platinum | Premium+ | Lounge-heavy flyers who use every credit | Broadest lounge network | None |

| Venture X | Premium | Simple premium perks, low maintenance | Yes | None |

Treat this as a starting frame, not a verdict. Fees, credits, and lounge networks change, so check each issuer before applying.

No foreign transaction fee as a baseline for trips

If you take even one international trip a year, a card with no foreign transaction fee should be your default for purchases abroad. The typical fee is a few percent on every charge in another currency, and it adds up fast across a trip. All four cards above waive it, which is part of why they qualify as travel cards in the first place.

You do not need a premium card to skip the fee. Plenty of no-fee and mid-tier cards waive it too, so a budget traveler can build a fee-free travel wallet without paying a premium annual fee. Our roundup of credit cards with no foreign transaction fee 2026 covers cheaper options if you only travel occasionally.

One more habit that saves money abroad: when a terminal asks whether to charge you in U.S. dollars or the local currency, choose local. Paying in dollars triggers dynamic currency conversion, which usually bakes in a worse exchange rate than your card would apply on its own.

Common questions

Is a premium travel card worth the annual fee?

It depends on how much of the card's credits and perks you will actually use. Add up the travel credits, lounge value, and protections you will genuinely claim, subtract the fee, and see whether you come out ahead before counting points. If you travel rarely, a no-fee or mid-tier card often makes more sense.

What is the difference between points and miles on these cards?

Bank points such as Chase, Amex, and Capital One rewards are flexible — you can transfer them to airline and hotel partners or redeem for travel directly. Airline miles tie you to one program. Transferable points give more options but take more learning to use well.

Can I have more than one travel card?

Yes, and many travelers pair a premium card for credits and lounges with a no-fee card for everyday or backup spending. Just make sure each annual fee is justified by perks you use, and watch issuer application rules before opening several cards in a short window.

Do travel cards help if I do not travel much?

Usually not enough to justify a premium fee. If you fly once or twice a year, a card with no annual fee, no foreign transaction fee, and flexible rewards often beats a premium card whose credits you will not use.

Last updated: June 2026. Rates, fees, and issuer rules change — confirm current terms before you apply or transfer a balance. This is general information, not personal financial advice.

Tired of receiving your unsolicited mail, time for you to cease sending your mail. If I need a credit card I will ask for it on my own time.

hey there.. please call capital one at 1-877-383-4802 and tell them you would like your information removed from their system and no more mailings