The Capital One Venture X and the Chase Sapphire Preferred sit at two different price points, and the choice usually comes down to how you value annual credits against transfer partners. Venture X carries a premium fee that it tries to win back with travel statement credits and lounge access. Sapphire Preferred keeps its fee low and leans on flexible points and a strong list of airline and hotel partners. This comparison walks through fees, earning, lounges, redemption, and the kind of traveler each card actually fits. Exact dollar amounts, bonus offers, and credit terms change, so confirm the current details on each issuer's page before you apply.

Annual fee and travel credits

The clearest difference between these two cards is the annual fee. Venture X is a premium card with a fee that runs several times higher than the Sapphire Preferred's. In exchange, Capital One bundles in recurring credits — typically an annual travel statement credit when you book through its travel portal, plus a yearly bonus of miles on your account anniversary. If you book travel through that portal every year, the credit and anniversary miles can offset much of the fee, which changes the real cost of holding the card.

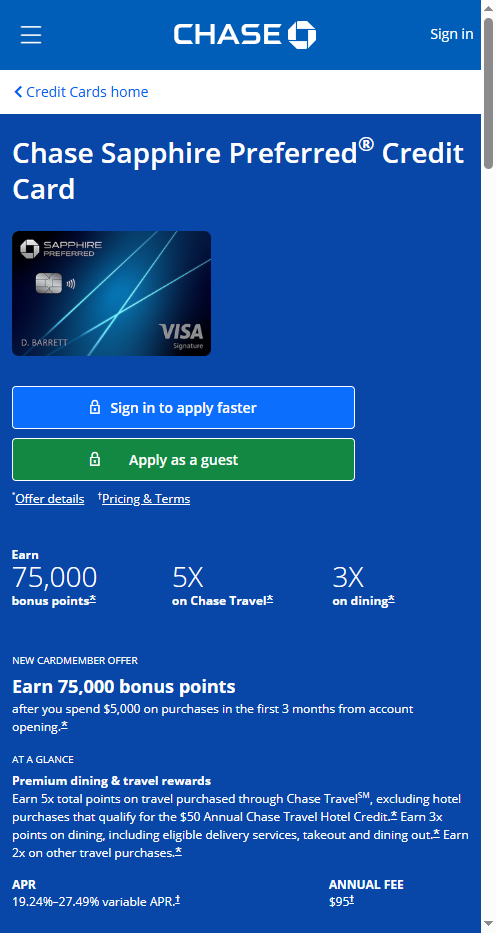

Sapphire Preferred takes the opposite approach. The fee is modest, and instead of large statement credits it offers smaller perks like a hotel credit and an annual points bonus tied to your spending. Because the fee is low, you do not have to chase credits to justify keeping the card open year after year. For a deeper look at where Sapphire Preferred fits in Chase's lineup, see our guide to the best Chase credit cards.

One practical point: Venture X credits are only worth their face value if you would have booked through the issuer's portal anyway. If you prefer booking directly with airlines and hotels, those credits are easier to leave on the table, and the math tilts back toward the lower-fee card.

Earning structure compared

Both cards earn transferable points, but they reward different spending. Venture X earns a flat rate on most everyday purchases, with higher rates on travel booked through Capital One Travel. That flat base rate is appealing if your spending is spread across many categories and you do not want to track bonus tiers.

Sapphire Preferred is more category-driven. It pays elevated points on travel and dining, with extra weight on certain bookings made through Chase Travel and on streaming or online grocery in some versions. If a large share of your monthly spend is restaurants and trips, the bonus categories can out-earn a flat rate. Here is a simplified side-by-side of how the two tend to be structured — verify current rates on each issuer's page, since these are adjusted periodically.

| Feature | Capital One Venture X | Chase Sapphire Preferred |

|---|---|---|

| Annual fee | Premium (higher) | Modest (lower) |

| Base earning | Flat rate on most purchases | Category bonuses (travel, dining) |

| Travel-portal bonus | Highest rate via Capital One Travel | Elevated rate via Chase Travel |

| Recurring credits | Travel credit + anniversary miles | Hotel credit + points bonus |

| Lounge access | Yes (Capital One + Priority Pass) | No standalone lounge access |

| Points type | Miles, transferable | Ultimate Rewards, transferable |

For a wallet that spends heavily and broadly, the flat rate plus credits can pull ahead. For a wallet centered on dining and travel, the category bonuses can win even at the lower fee.

Lounge access and protections

Lounge access is where Venture X separates itself. The card includes access to Capital One's own lounge network and a Priority Pass membership, usually with guest privileges that depend on the current terms. If you fly several times a year and value a quiet seat and free food before a flight, that benefit alone can be worth a meaningful share of the fee.

Sapphire Preferred does not include standalone lounge access. That is a deliberate trade — it keeps the fee low. If lounges matter to you and you want to stay in the Chase ecosystem, the comparison shifts toward the Reserve tier instead, which we cover in our Sapphire Preferred vs Reserve guide.

On protections, both cards carry travel and purchase coverage that tends to be stronger than a no-fee card. Expect items like trip cancellation or delay protection, some rental car coverage, and extended warranty or purchase protection on eligible buys. The exact coverage limits and exclusions differ and are updated over time, so read the benefits guide for the specific card before you rely on any single protection.

Transfer partners and redemption flexibility

This is the heart of the decision for many travelers. Both cards let you transfer points to airline and hotel partners, which is where outsized value usually comes from. The partner lists overlap on some programs but not all, so the right card can depend on which loyalty programs you actually use.

- Chase Ultimate Rewards is known for a deep bench of airline and hotel partners and strong portal redemption value on premium tiers.

- Capital One miles transfer to a wide set of airline partners as well, often at a 1:1 rate, and the program has expanded its list over the years.

- Both let you redeem against travel as a statement credit or through their own travel portals, though transfers to partners typically stretch points further on premium-cabin awards.

If you already have a favorite frequent-flyer program, check which card transfers to it before anything else. A single partner you fly often can outweigh small differences in fees or earning rates. If you are still building your strategy, our overview of the best Capital One credit cards explains how the miles ecosystem fits together.

Who should choose Venture X vs Preferred

Choose Venture X if you travel enough to use the lounge access and the annual travel credit, and if you prefer a flat earning rate without tracking categories. The premium fee makes sense when the credits and lounge visits add up to more than the fee, which is realistic for frequent flyers who book through the issuer's portal.

Choose Sapphire Preferred if you want a low fee, you spend heavily on dining and travel, and you value Chase's transfer partners over lounge access. It is also the more forgiving choice for someone who travels a few times a year rather than constantly, because there is less fee to justify.

A quick way to decide: add up the credits and lounge value you would genuinely use with Venture X. If that total comfortably clears the fee gap between the two cards, Venture X is likely the better deal. If not, Sapphire Preferred keeps more money in your pocket while still giving you transferable points. Keep in mind that Chase applies its 5/24 rule to most personal cards, which can affect whether you are approved for the Preferred.

Common questions

Is Venture X worth the higher annual fee?

It can be if you use the annual travel credit, collect the anniversary bonus, and visit lounges a few times a year. Those benefits often offset much of the fee for frequent travelers. If you rarely book through the issuer's portal or skip lounges, the lower-fee Sapphire Preferred may be the better value. Confirm current credit amounts on the issuer site.

Can I transfer points between these two cards?

No. Capital One miles and Chase Ultimate Rewards are separate programs and do not transfer to each other. Each card transfers only to its own list of airline and hotel partners, so check which partners each program supports before you decide.

Which card earns more on everyday spending?

Venture X uses a flat rate on most purchases, which suits broad, mixed spending. Sapphire Preferred pays bonus rates on travel and dining, so it can earn more if those categories dominate your budget. The best earner depends on where your money goes each month.

Does Chase 5/24 affect the Sapphire Preferred?

Yes. Chase generally declines applicants who have opened five or more personal cards from any issuer in the past 24 months. Capital One does not use the same rule, though it has its own approval criteria. Check your recent account history before applying for the Preferred.

Last updated: June 2026. Rates, fees, and issuer rules change — confirm current terms before you apply or transfer a balance. This is general information, not personal financial advice.

Tired of receiving your unsolicited mail, time for you to cease sending your mail. If I need a credit card I will ask for it on my own time.

hey there.. please call capital one at 1-877-383-4802 and tell them you would like your information removed from their system and no more mailings