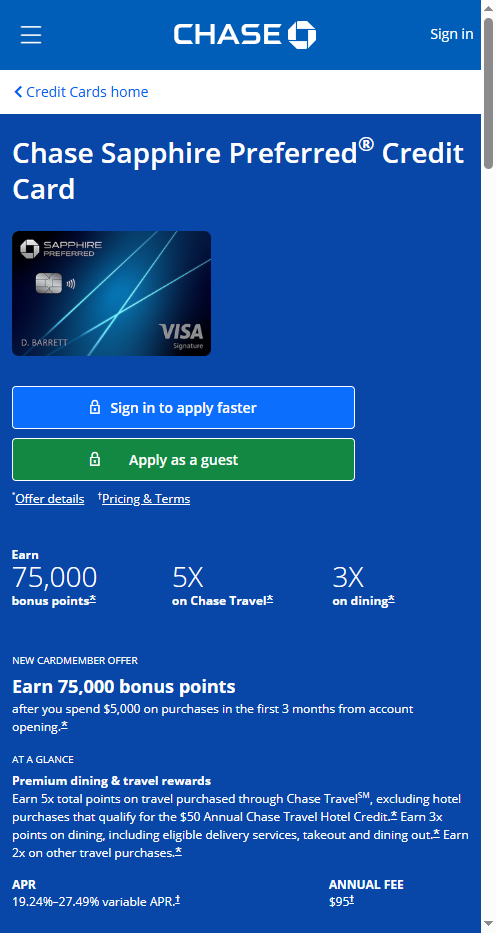

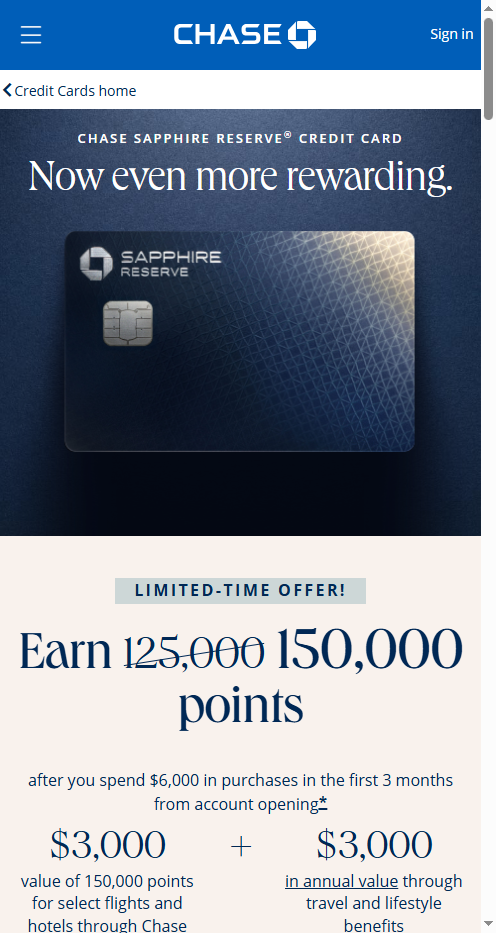

Both Sapphire cards earn Chase Ultimate Rewards points and let you transfer to the same airline and hotel partners, so the real question is how much annual fee you want to pay and how often you actually travel. The Preferred is the mid-tier travel card most people start with; the Reserve is the premium tier with lounge access and a larger travel credit. This page lines them up side by side so you can see which tier earns back its fee for your spending.

Fees and travel credits at a glance

The headline difference is the annual fee. The Reserve costs several times more per year than the Preferred, and it offsets part of that with a yearly travel credit that the Preferred does not match. Chase changes the exact numbers from time to time, so treat the figures below as the structure rather than the precise dollar amounts and confirm current terms on the issuer page before you apply.

| Feature | Sapphire Preferred | Sapphire Reserve |

|---|---|---|

| Annual fee | Lower mid-tier fee | Higher premium fee |

| Annual travel credit | None | Yes, applied to travel purchases |

| Lounge access | No | Yes (airport lounge network) |

| Foreign transaction fee | None | None |

| Points transfer partners | Same as Reserve | Same as Preferred |

The travel credit matters because it reduces the effective fee. If you reliably spend on flights or hotels each year, the Reserve's credit can wipe out a large slice of its sticker price before you count any points.

Earning rates and transfer partners

Both cards earn extra points on travel and dining and a base rate on everything else, with the Reserve generally earning more per dollar in its bonus categories. Where they are identical is the back end: points from either card move to the same set of airline and hotel transfer partners at a 1:1 ratio, so a frequent flyer is not locked into one tier to reach a given program.

The other lever is redemption value through the Chase travel portal. Each tier applies its own multiplier when you book travel directly through Chase rather than transferring out. That portal bonus is one reason the Reserve can stretch points further, but transferring to partners is usually where the highest value lives for both cards. For a wider look at how these stack against non-Chase options, see our roundup of the best travel credit cards for 2026.

- Everyday spend: both earn a base rate; neither is the best choice for non-bonus categories.

- Travel and dining: Reserve typically earns a higher multiplier than Preferred.

- Transfers: identical partner list, so the points themselves are equally flexible.

Lounges and protections — Reserve only?

Lounge access is the clearest line between the two. The Reserve includes membership in an airport lounge network and access to Chase's own lounge locations; the Preferred includes neither. If you spend real time in airports, that perk alone can justify the higher tier.

Travel protections are more nuanced. Both Sapphire cards carry a strong set of insurance benefits — trip cancellation and interruption coverage, baggage protection, and primary rental car coverage among them — and the Preferred is well known for offering meaningful protection at a lower fee. The Reserve tends to carry higher coverage limits on some of those benefits. Read the current benefits guide for each card before relying on any single protection, since limits and exclusions change. If you want the full current breakdown of the top tier, our page on Chase Sapphire Reserve benefits goes deeper.

Net annual cost worked example

The honest way to compare premium cards is net cost: the annual fee minus the credits you would actually use. A perk you forget to redeem is not a discount.

- Start with the fee. Write down the current annual fee for each card from the Chase site.

- Subtract credits you will truly use. For the Reserve, subtract the travel credit only if you book qualifying travel every year anyway. The Preferred has no such credit to subtract.

- Add the value of lounge visits. Estimate what you would otherwise pay for lounge day passes, then count only the Reserve.

- Compare the remainder. If the Reserve's net cost after credits and lounge value is close to the Preferred's fee, and you travel often, the Reserve usually wins. If you barely travel, the Preferred's lower fixed fee is hard to beat.

The point of the exercise is that the Reserve only looks expensive on paper. For a steady traveler who uses the credit and the lounges, the gap between the two cards shrinks far more than the fee difference suggests. For someone who takes one or two trips a year, the credits go unused and the Preferred is the cheaper, simpler choice.

Which card to get first

If this is your first Sapphire card and you are not yet sure how much you travel, start with the Preferred. It carries the lower fee, the same transfer partners, and most of the protections that make the Sapphire line useful. You can product-change to the Reserve later if your travel habits grow, often without a new application.

Go straight to the Reserve when you already travel enough to use the annual travel credit and visit airport lounges several times a year. At that level of travel the credit and lounge access can cover most of the fee gap, and the higher earning rate does the rest.

One application note for both: Chase's 5/24 guideline means it may decline you if you have opened too many new cards across all issuers in the last 24 months. Check that before applying so you do not waste a hard inquiry. For how the Sapphire cards fit alongside Freedom and Ink, see our overview of the best Chase credit cards.

Common questions

Can I have both the Preferred and the Reserve at the same time?

Generally no. Chase typically lets you hold only one Sapphire card at a time, so most people choose one tier or move between them by product change rather than carrying both.

Do points from the Preferred and Reserve transfer to the same partners?

Yes. Both earn Chase Ultimate Rewards and transfer 1:1 to the same airline and hotel partners. The difference is in earning rates and in the portal redemption multiplier, not in which partners you can reach.

Is the Reserve worth the higher fee?

It depends on how much you travel. If you use the annual travel credit and the lounge access, the net cost after those benefits can land close to the Preferred's fee. If you rarely fly, the credits go unused and the Preferred is the better value.

Can I upgrade from Preferred to Reserve later?

Often yes, through a product change within Chase rather than a brand-new application. Terms and any bonus eligibility differ for upgrades, so confirm the current rules with Chase before you switch.

Last updated: June 2026. Rates, fees, and issuer rules change — confirm current terms before you apply or transfer a balance. This is general information, not personal financial advice.

Tired of receiving your unsolicited mail, time for you to cease sending your mail. If I need a credit card I will ask for it on my own time.

hey there.. please call capital one at 1-877-383-4802 and tell them you would like your information removed from their system and no more mailings