Capital One sells two very different cards under one roof. The Venture X is a premium travel card built around an annual travel credit and lounge access, while the Savor is a no-fee card aimed at people who spend most of their money on food and going out. They earn in different ways, they cost different amounts, and they reward different lifestyles. This breakdown looks at how each one works, what they cost, and whether keeping both in the same wallet actually makes sense.

Venture X — travel credits and lounges

The Venture X is Capital One's premium travel card. It carries an annual fee, and its value depends on whether you use the benefits attached to it rather than just chasing points. The card earns miles on everyday spending, with a higher rate on travel booked through Capital One Travel, and those miles can be redeemed for travel or transferred to airline and hotel partners.

Two features carry most of the weight here:

- An annual travel credit applied to bookings through Capital One Travel. If you book flights or hotels through that portal, the credit offsets a large part of the annual fee.

- Lounge access through Capital One Lounges and partner networks, usually extended to the cardholder and a number of guests, plus an airport experience membership.

The math is simple to test before you apply. Add up the travel credit and the lounge visits you would realistically use in a year. If that total clears the annual fee, the card pays for itself; the miles you earn on top are the actual profit. If you rarely fly or never set foot in a lounge, the fee works against you. Exact credit amounts, earn rates, and any current offer vary, so confirm the numbers on the issuer page before deciding.

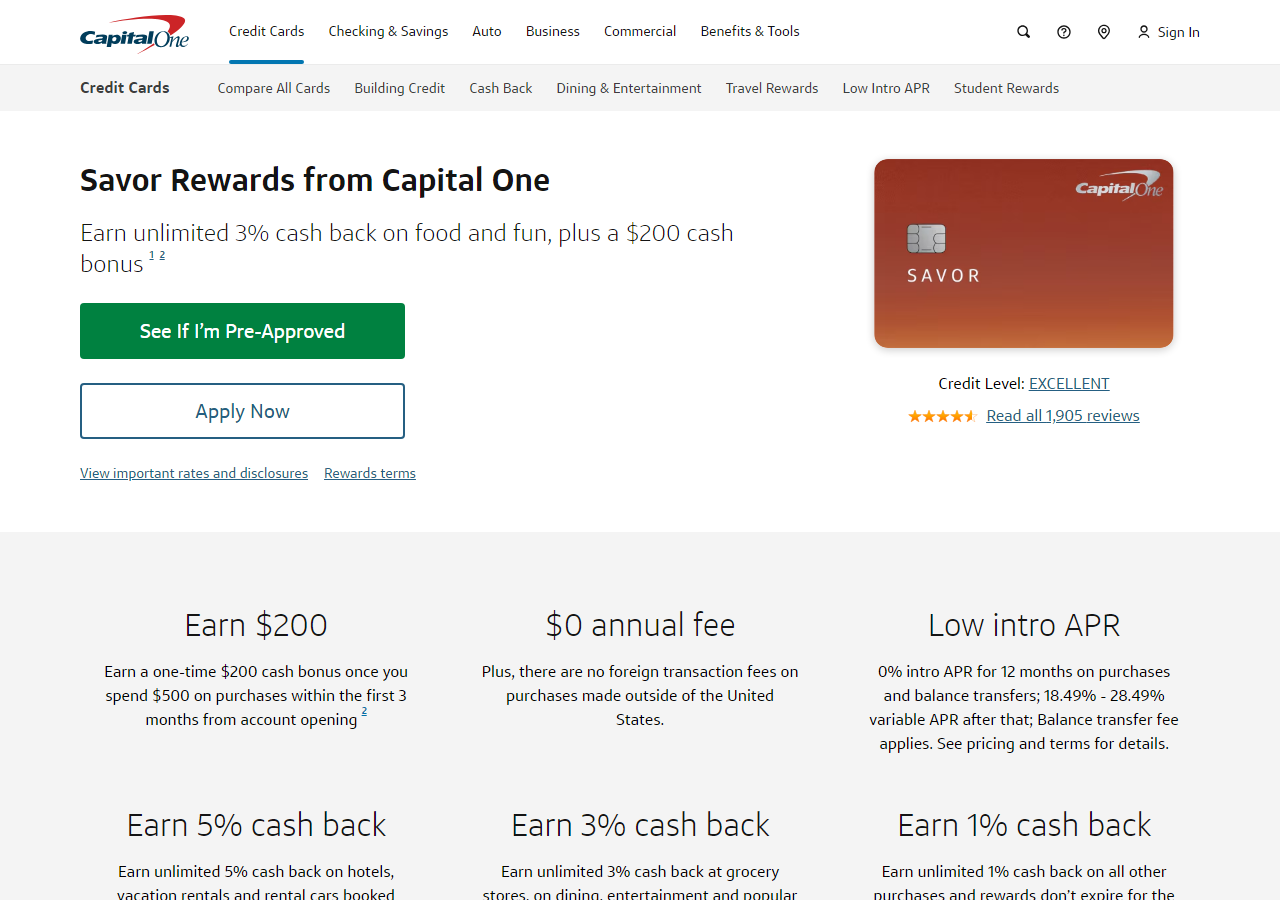

Savor — dining and entertainment

The Savor is the opposite kind of card. It is built for cash back on the categories where casual spenders actually put money: restaurants, entertainment, popular streaming services, and grocery stores, with a flat base rate on everything else. There is no premium travel machinery to manage — you swipe, you earn cash back, and you redeem it.

This makes the Savor easy to value. You do not need a spreadsheet of lounge visits or portal bookings. If a meaningful share of your monthly spending is dining and going out, the elevated cash-back rate does the work on its own. It is a strong everyday card for someone who eats out often, splits restaurant tabs, or pays for a stack of streaming subscriptions, and it pairs naturally with other dining-focused options covered in our guide to the best credit cards for restaurants in 2026.

What the Savor does not give you is travel infrastructure. There is no lounge access and no annual travel credit, so a frequent flyer who values airport perks will find it thin. Reward percentages and category definitions can change, so check the current terms on Capital One's site before you count on a specific rate.

Annual fees compared

The clearest difference between these two cards is what they cost to hold. The table below frames the trade-off; treat the specifics as a model rather than exact figures, since fees and benefits change.

| Feature | Venture X | Savor |

|---|---|---|

| Card type | Premium travel (miles) | Everyday cash back |

| Annual fee | Yes — higher | No annual fee |

| Top earn category | Travel via Capital One Travel | Dining and entertainment |

| Travel credit | Yes, annual | No |

| Lounge access | Yes | No |

| Best for | Frequent travelers | Diners and casual spenders |

An annual fee is not automatically bad. A travel card with a fee can be cheaper to own than a free card if its credits and access exceed what you pay. The question is not whether the Venture X has a fee — it is whether your usage cancels that fee out. For the Savor, there is no break-even to calculate, which is part of its appeal.

Can you justify both?

Holding both cards is a real strategy, not redundancy, because they cover separate categories. The Savor earns on dining and entertainment; the Venture X earns on travel and unlocks lounges and a travel credit. Used together, you route restaurant and going-out spending to the Savor and travel spending to the Venture X, and the categories barely overlap.

Both make sense when you both travel enough to use the Venture X benefits and spend enough on food to make the Savor's cash back add up. Capital One miles and cash back live in the same ecosystem, which makes a two-card setup straightforward to manage. The decision usually comes down to two questions:

- Will you use enough Venture X travel credit and lounge visits each year to cover its fee?

- Is a real share of your monthly spending dining and entertainment?

Two clear yeses point to keeping both. If only one is true, carry the single card that matches your spending and skip the other. For a wider view of where each Capital One product fits, see our roundup of the best Capital One credit card options.

Quicksilver as a third no-fee layer

There is a third Capital One card worth knowing about when you build this stack: the Quicksilver. It is a no-annual-fee card with a flat cash-back rate on every purchase, with no categories to track. That makes it the natural catch-all for spending that does not fall into dining, entertainment, or travel.

A three-card setup inside one issuer can look like this:

- Savor — dining, entertainment, streaming, groceries.

- Venture X — flights, hotels, and anything booked through Capital One Travel, plus lounge access.

- Quicksilver — everything else, at a flat rate, with no fee.

You do not need all three to start. Most people begin with the one card that matches the bulk of their spending and add layers only when the second category becomes large enough to justify another account. Keeping the cards with the same issuer also makes it easier to manage rewards in one place.

Common questions

Is the Venture X worth the annual fee?

It is worth it if the value of the annual travel credit plus the lounge visits you actually use is greater than the fee. Add those up against your real travel habits before applying, and confirm current credit and fee amounts on Capital One's site, since they change.

Can I have both the Venture X and the Savor?

Yes. They earn in different categories — travel versus dining and entertainment — so they complement each other rather than compete. Approval depends on Capital One's own rules and your credit profile.

Does the Savor charge an annual fee?

The Savor is positioned as a no-annual-fee cash-back card, but card terms can change. Verify the current fee and reward categories on the issuer page before you apply.

Where does the Quicksilver fit in?

The Quicksilver is a flat-rate, no-fee card for purchases that do not earn bonus rewards on the Savor or Venture X. It works as a simple catch-all in a multi-card Capital One setup.

Last updated: June 2026. Rates, fees, and issuer rules change — confirm current terms before you apply or transfer a balance. This is general information, not personal financial advice.

Tired of receiving your unsolicited mail, time for you to cease sending your mail. If I need a credit card I will ask for it on my own time.

hey there.. please call capital one at 1-877-383-4802 and tell them you would like your information removed from their system and no more mailings