The Chase Freedom Unlimited and the Chase Freedom Flex are two no-annual-fee cash-back cards that look similar on a shelf and behave very differently in a wallet. One pays a steady rate on everything. The other pays a high rate on a short list of categories that change every three months, but only after you remember to turn them on. Knowing which one fits your spending — or whether you should carry both — comes down to how much effort you want to put into chasing categories.

Freedom Unlimited — flat earning

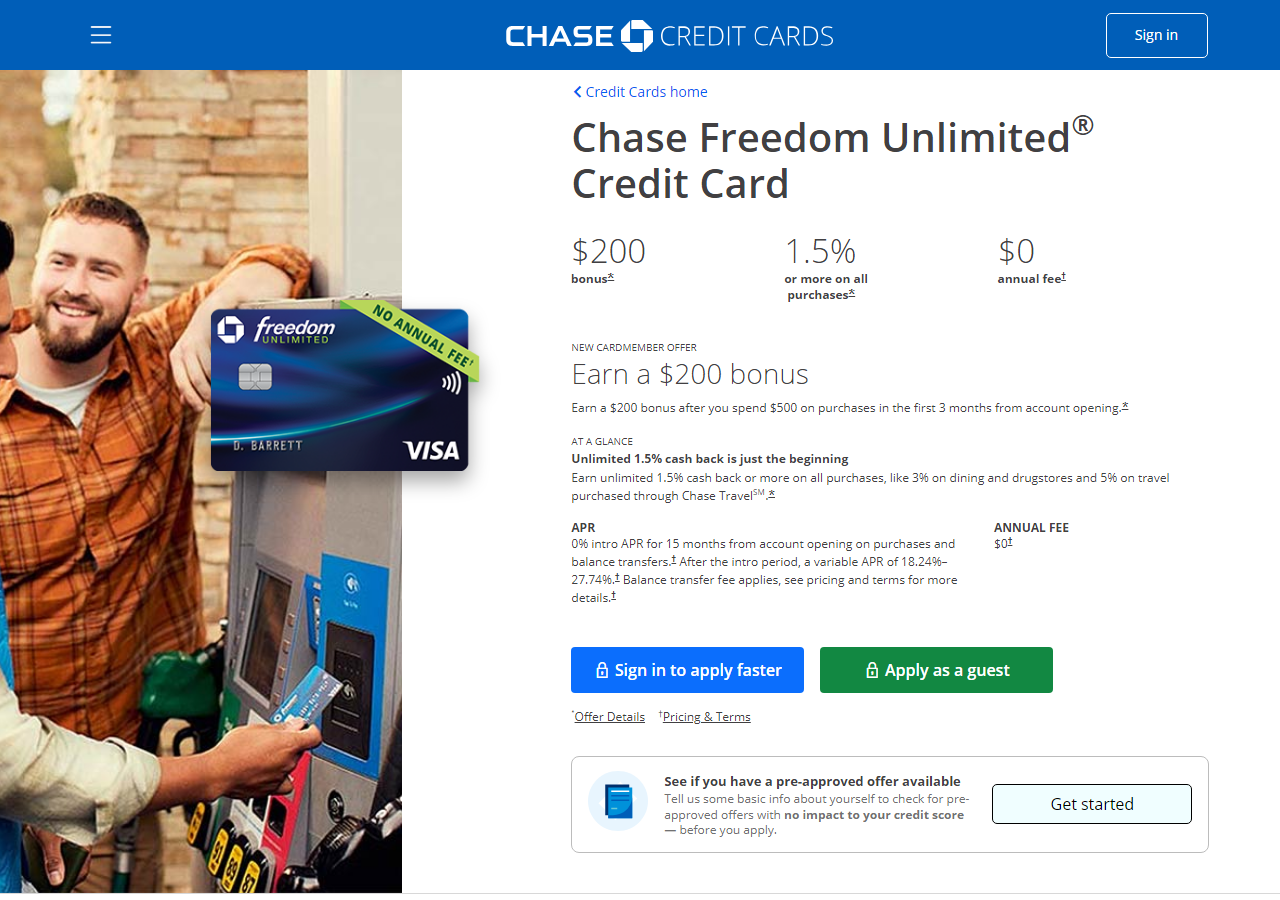

The Freedom Unlimited is the set-and-forget option. It earns a flat rate on every purchase with no categories to track and no quarters to activate, plus elevated rates on a few areas such as dining and drugstores and a higher rate on travel booked through Chase Travel. Exact rates can change, so confirm the current numbers on the issuer site before you apply.

This card rewards consistency more than strategy. If most of your spending is spread across general merchants — online shopping, home goods, gas, subscriptions, the kind of purchases that never neatly fit a category — a flat rate often beats a rotating bonus you forget to claim. There is no cap on the base rate, so a single large purchase earns the same as a hundred small ones.

- No annual fee.

- One flat rate on all non-bonus spending, unlimited.

- No activation, no category calendar.

- Higher rates on dining, drugstores, and Chase Travel bookings.

Freedom Flex — categories and rotation

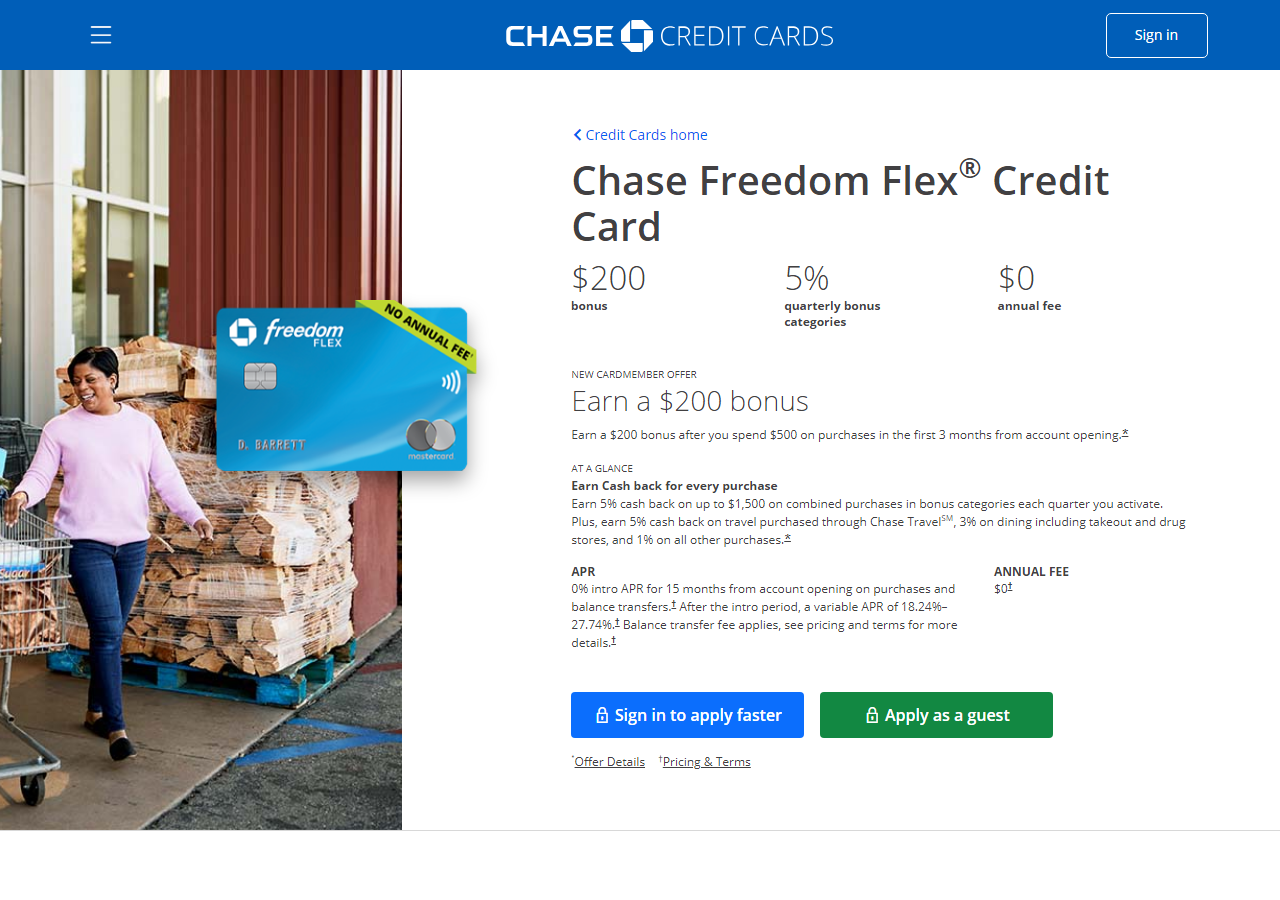

The Freedom Flex is built around rotating bonus categories. Each quarter Chase publishes a new set of categories — common examples over the years have included grocery stores, gas stations, streaming, wholesale clubs, and online retailers — that earn a high cash-back rate up to a spending cap. On top of the rotating tier, the Flex pays elevated rates on dining, drugstores, and travel booked through Chase Travel, so it keeps earning even between strong quarters.

The catch is two-fold: the categories change four times a year, and the high rate applies only after you activate it for the quarter. Miss the activation and that quarter's purchases drop to the base rate. The Flex is best for people who don't mind a small recurring task in exchange for a meaningfully higher return on targeted spending.

Activation and quarterly caps

Activation is the single biggest practical difference between these two cards. The Freedom Unlimited never asks anything of you. The Freedom Flex asks you to opt in each quarter, usually through your online account, the Chase app, or an email link Chase sends near the start of the quarter.

Two rules are worth keeping in mind:

- The bonus rate is capped. The high rotating rate applies only up to a set amount of combined spending per quarter. Beyond that cap, those purchases earn the base rate. Plan large category purchases so they land inside the cap.

- Activation is not retroactive past the quarter. If you activate mid-quarter, earlier purchases in that quarter may still count once you opt in, but a quarter you never activate is simply gone. Set a recurring calendar reminder for the first week of January, April, July, and October.

If remembering four dates a year sounds like a chore you will lose, that honest answer points you toward the Unlimited.

Using both cards together

Because both cards carry no annual fee, many people hold both and let each do what it does best. The routine is simple: put category spending on the Flex during quarters that match your habits, run everything else through the Unlimited's flat rate, and lean on whichever card has the better elevated rate for shared categories like dining and drugstores in any given quarter.

| Feature | Freedom Unlimited | Freedom Flex |

|---|---|---|

| Annual fee | None | None |

| Base earning | Flat rate on everything | Base rate outside bonuses |

| Bonus structure | Fixed elevated categories | Rotating quarterly + fixed categories |

| Activation needed | No | Yes, each quarter |

| Spending cap on top rate | No cap on base | Quarterly cap on rotating bonus |

| Best for | Hands-off, broad spending | People who track categories |

Both cards earn the same type of Chase points, so rewards from one can be combined with the other in a single account. For a wider view of how these fit alongside the rest of the lineup, see our overview of the best Chase credit cards, and if a yearly charge is a dealbreaker for you, compare them against other no-annual-fee cards.

Transfer to Sapphire — when it matters

On their own, the Freedom cards redeem their points as cash back at a fixed value. The points become more interesting if you also hold a premium Chase travel card such as a Sapphire product. With that card in your account, you can move Freedom points over and redeem them for travel — often at a higher value through the travel portal, or by transferring to airline and hotel partners where the value can be higher still.

This only matters if you actually travel and are willing to manage the extra card, which typically carries an annual fee. If you redeem everything as cash, the transfer path adds nothing for you, and the Freedom cards stand fine on their own. Treat the Sapphire link as an optional upgrade to your points, not a requirement.

Common questions

Can I have both the Freedom Unlimited and the Freedom Flex?

Yes. They are separate products with separate credit lines, and because neither charges an annual fee, holding both is common. Approval still depends on Chase's overall card policies and your credit profile, so confirm eligibility on the issuer site.

What happens if I forget to activate the Flex categories?

Purchases in that quarter's bonus categories earn the card's base rate instead of the high rotating rate until you activate. A quarter you never activate at all earns only the base rate on those categories. Set a quarterly reminder to avoid leaving rewards on the table.

Which card earns more overall?

It depends on your spending. If a large share of your purchases falls into the rotating categories and you activate reliably, the Flex can earn more. If your spending is broad and unpredictable, the Unlimited's flat rate usually wins with no effort. Many people simply carry both.

Do the points expire?

Chase points generally remain available as long as the account is open and in good standing, but terms can change. Always check the current rewards program rules on the issuer site before counting on long-term value.

Last updated: June 2026. Rates, fees, and issuer rules change — confirm current terms before you apply or transfer a balance. This is general information, not personal financial advice.

Tired of receiving your unsolicited mail, time for you to cease sending your mail. If I need a credit card I will ask for it on my own time.

hey there.. please call capital one at 1-877-383-4802 and tell them you would like your information removed from their system and no more mailings